A glimpse of Spring in August’s numbers - REINZ stats August 2023

Thursday, 14 September 2023

By continuing, you agree to our terms of use and privacy policy

Instructions on how to reset your password will be sent to the email below.

Your password reset link has been sent. Please check your inbox and follow the instructions provided.

Thursday, 14 September 2023

In August 2023, the New Zealand property market showed optimism and increased activity, despite a shortage of property listings. Sales counts rose compared to the previous year and month, with Auckland and other regions experiencing sales growth. Median days to sell decreased, and while the total number of properties for sale declined, new listings increased, indicating growing seller confidence. The national median sale price decreased year-on-year, except for a few regions. Overall, the market appears to have stabilized, with some signs of recovery. However, the Housing Price Index (HPI) remains below its peak.

Regional highlights

- Nelson (0.7%), Canterbury (0.8%), Southland (2.0%), Northland (3.6%) and Gisborne (14.8%) saw an increase in median sale price year-on-year with Gisborne also up 13.0% month-on-month.

- Southland had the biggest month-on-month increase in sales count with a 25.5% rise and a 4.2% increase year-on-year, followed by Manawatu-Wanganui with a 20.5% increase month-on-month and an 8.6% increase year-on-year.

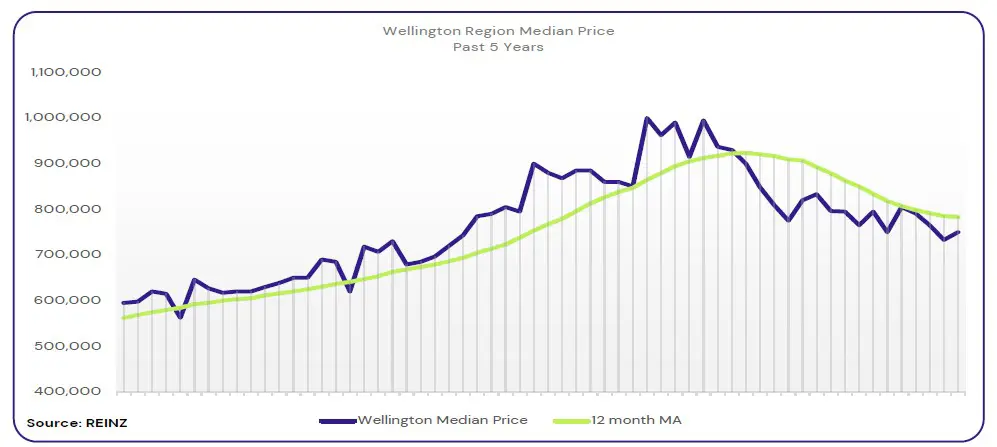

- Wellington saw increases in median sale price up 2.3% from $733,000 to $750,000, a 16.9% increase in the number of properties sold from 438 to 512 and a decrease in the days to sell from 52 to 38, a 14-day decrease.

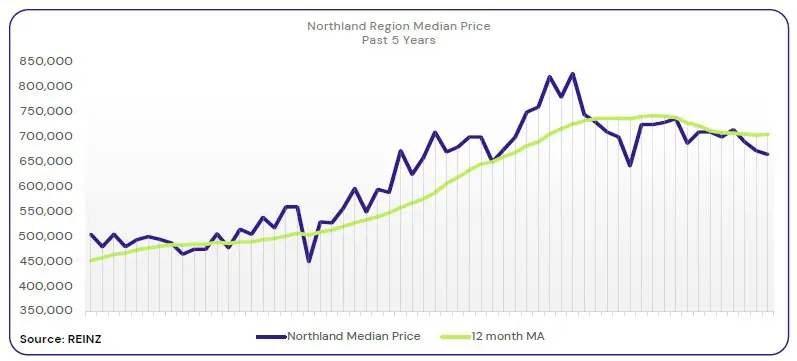

In Northland, median prices increased by 3.6% year-on-year to $665,000.

“First-home buyers continued to be the most active buyer group in Whangarei, with activity from investors still going strong. In Kerikeri, owner-occupiers continued to be the most active. Most vendors have adjusted their price expectations based on the current market, with a few holding on to their original prices.

Open home attendance saw encouraging numbers, mainly due to spring arriving along with warmer weather. Activity in Whangarei auction rooms continued to rise.

Uncertainty about interest rates, lending criteria, and anticipation of the election continues to influence decision making. Local salespeople report that enquiries are being made, however, buyers are waiting for more favourable conditions. Local agents are cautiously optimistic and believe the market is heading in a positive direction as the seasons change.” (REINZ)

The current median Days to Sell of 61 days is more than the 10-year average for August which is 55 days. There were 45 weeks of inventory in August 2023 which is 8 weeks more than the same time last year.

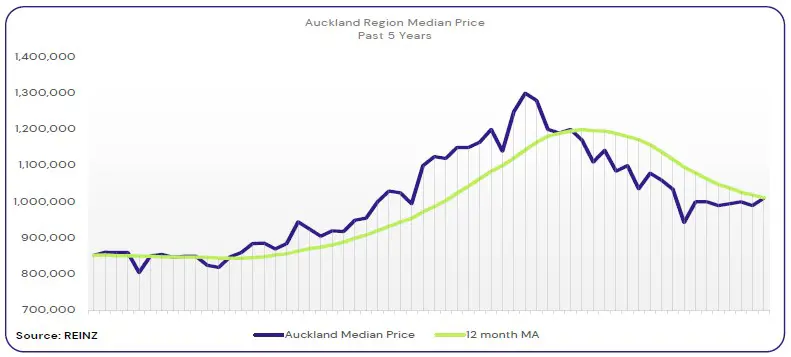

Auckland’s median prices decreased by 8.2% year-on-year to $1,010,000.

“Owner occupiers were the most active buyers in North and Central Auckland; Central and South Auckland also saw some activity from first-home buyers. Developers continue to show interest in South Auckland. Some vendors have adjusted their price expectations, while others are holding on to their original expectations. Central Auckland agents have been working on helping vendors understand current market conditions.

Open homes and auction rooms across Auckland saw slight to moderate increase in attendance. Sales counts increased in South Auckland, were lower yet stable in Central Auckland, and were low in North Auckland compared to previous years.

The market saw some improvement in South Auckland and some activity in Central Auckland, though not as much as in previous years. Interest rates, lending criteria, and the election continue to influence the market.” (REINZ)

The current median Days to Sell of 41 days is more than the 10-year average for August which is 3 days. There were 25 weeks of inventory in August 2023 which is 7 weeks less than the same time last year.

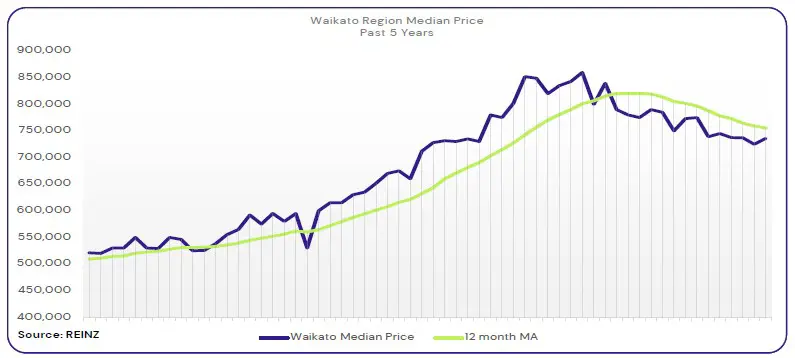

In the Waikato, median prices decreased by 5.6% year-on-year to $736,000.

“First-home buyers and owner occupiers were the most active buyer groups. Thames-Coromandel also saw activity from holiday home buyers.

More vendors are adjusting their prices to meet the current market. Taupo salespeople believe the market will improve in spring and some are still hoping for better prices. Coromandel saw little activity at open homes, most likely due to continued challenges with road access following Cyclone Gabrielle. Hamilton and Taupo saw reasonable activity at open homes and a slight increase in activity in auction rooms.

Current economic conditions and anticipation of the election continue to impact the market. Coromandel’s market was also impacted by continued road infrastructure issues. Local agents are expecting a steady market for the next few months, followed by an increase in activity in spring and summer.” (REINZ)

The current median Days to Sell of 48 days is more than the 10-year average for August which is 41 days. There were 19 weeks of inventory in August 2023 which is 14 weeks less than the same time last year.

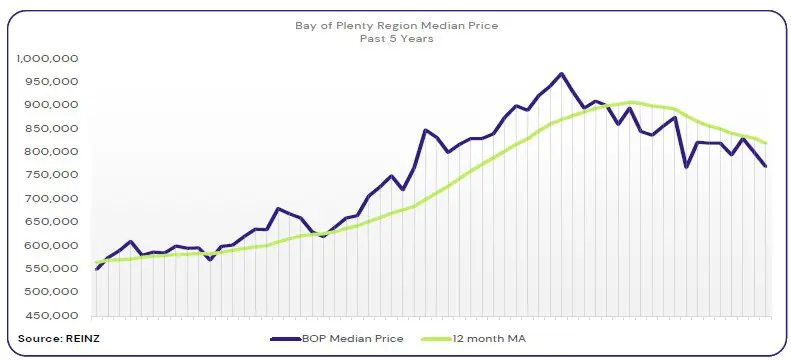

In Bay of Plenty, median prices decreased by 14.0% year-on-year to $770,000.

“First home buyers continued to be the most active buyer group in Tauranga and owner occupiers were the most active in Rotorua.

More vendors are willing to adjust their price expectations considering current market conditions, however there are still some who are holding on for more favourable conditions across the region.

Open home attendance picked up at some properties in Rotorua. New stock is attracting buyers in Tauranga, while listing decreased in Rotorua. Auction room activity saw a marked improvement and Tauranga sales counts lifted slightly.

Factors such as interest rates and the economic climate continue to shape market sentiment, with anticipation of the coming election playing a significant role. Local agents report the market is steady, with an optimistic feel about it.” (REINZ)

The current median Days to Sell of 54 days is more than the 10-year average for August which is 44 days. There were 24 weeks of inventory in August 2023 which is 1 week less than the same time last year.

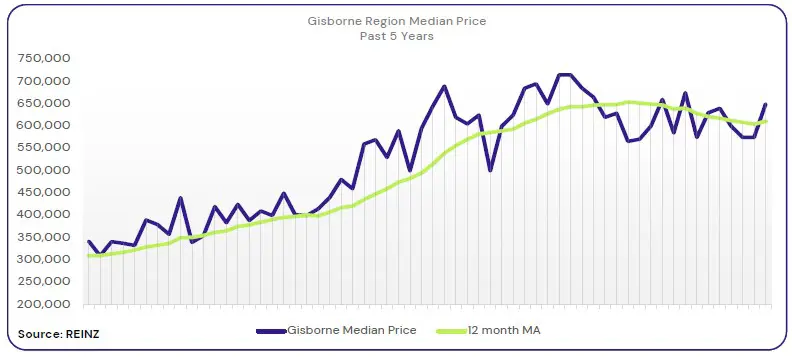

Median prices in Gisborne increased by 14.8% year-on-year to $650,000.

“Owner-occupiers and first-home buyers were the most active buyer groups in the region. Most vendors are meeting the market, yet some were still holding on for more favourable conditions. Open homes continued to see an increase in attendance; there was strong activity and active bidding at auctions.

The current economic conditions, low listing numbers, and anticipation of the election continued to impact market sentiment amongst both buyers and sellers. However local agents report that buyer activity has become more buoyant.” (REINZ)

The current median Days to Sell of 41 days is more than the 10-year average for August which is 37 days. There are 11 weeks of inventory in August 2023 which is 6 weeks less than last year.

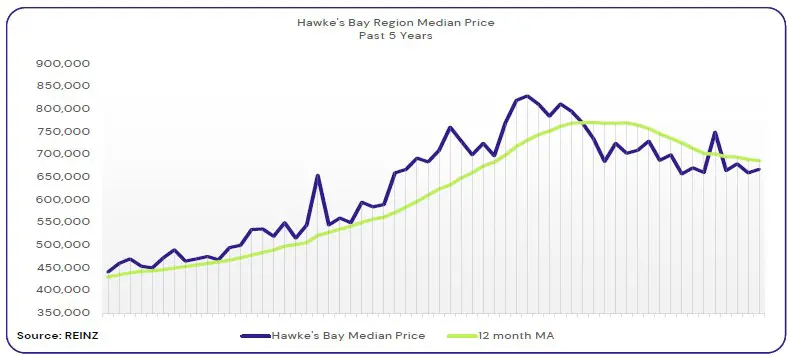

In Hawke’s Bay, median prices decreased by 5.0% year-on-year to $668,000.

First-home buyers and owner-occupiers were the most active buyer pool in the region. Most vendors are realistic with their price expectations, but some are staying firm to their initial expectations. Attendance at open homes picked up and sales numbers stayed steady.

Interest rates, cost of living, and other factors continue to impact the market. Local agents report that average listing numbers continue to decrease, with demand for entry level property demand remaining fairly strong. There is a sense that the market has bottomed out already and the discussion is now around how long it will take to see growth.” (REINZ)

The current median Days to Sell of 49 days is much more than the 10-year average for August which is 38 days. There were 17 weeks of inventory in August 2023 which is 2 weeks less than the same time last year.

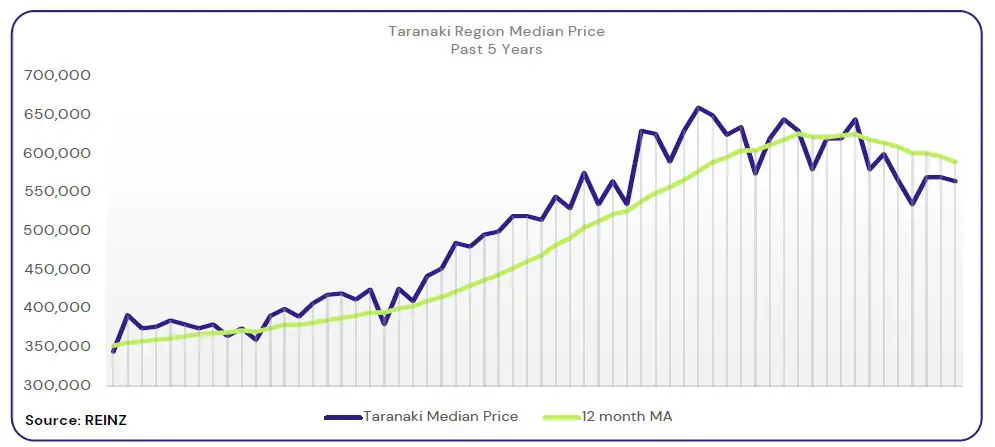

Taranaki’s median prices decreased by 12.4% year-on-year to $565,000.

“Owner-occupiers continued to be the most active buyers in the region, with some activity seen from first-home buyers. Investor activity remained low. Most vendors are adjusting their asking prices to reflect market conditions, and are aware of the additional time, on average, that a property may stay on the market.

Open-home attendance increased in August thanks to the improving weather. New listings that meet first-home buyer requirements were usually well attended.

Local salespeople report that it continues to be a buyers’ market in Taranaki, and many buyers have adopted a ‘wait and see’ approach. Local agents predict that the market will stay slow in anticipation of the coming election and are hopeful that spring will bring more activity from buyers.” (REINZ)

The current median Days to Sell of 48 days is much more than the 10-year average for August which is 38 days. There were 21 weeks of inventory in August 2023 which is 6 weeks more than the same time last year.

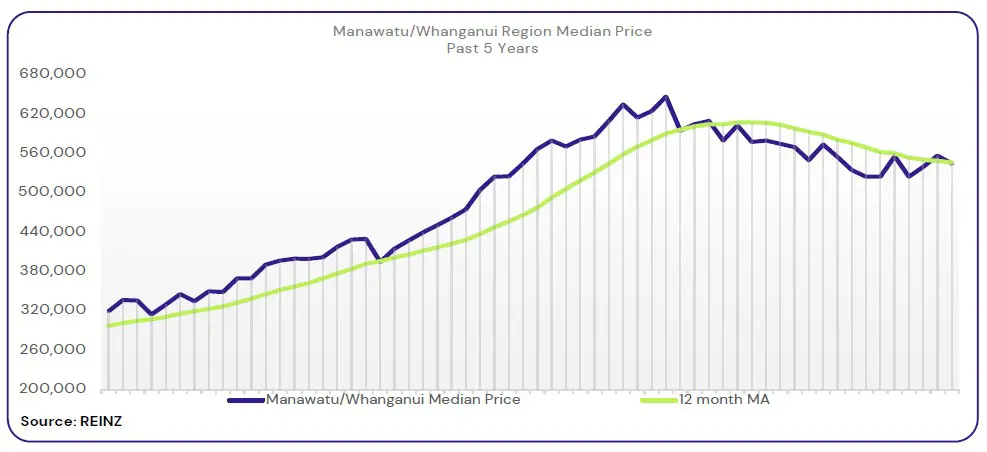

Median prices in Manawatu/Whanganui decreased by 5.2% year-on-year to $545,000.

“Owner-occupiers are still the most active buyer group, while the numbers for first-home buyers returning to the market continue to grow.

Vendors have adjusted their price expectations based on current market conditions. Open home attendance has been good at new listings and local agents report more first-home buyers viewing properties. Auction rooms have also seen some success in August.

Overall sales counts continued to decrease as buyers continued to be impacted by interest rates and a lack of listings. Anticipation of the upcoming election is also a factor.

Local salespeople predict that the market will remain the same for the next few months.” (REINZ)

The current median Days to Sell of 50 days is much more than the 10-year average for August which is 38 days. There were 23 weeks of inventory in August 2023 which is 3 weeks less than the same time last year.

Wellington’s median prices decreased by 3.2% year-on-year to $750,000.

“First-home buyers continued to be the most active buyer group, with some activity from investors as well. Vendors continued to set their price expectations to reflect current market conditions.

Local salespeople report steady attendance levels at open homes, with there being more success at private viewings. Auctions saw low levels of activity. Local agents say that the market is currently stable, with some signs of improvement in prices. Anticipation of the election continues to impact the market, but agents are hopeful that post-election and the arrival of spring, they will see more confidence in the market.” (REINZ)

The current median Days to Sell of 38 days is more than the 10-year average for August of 36 days. There were 11 weeks of inventory in August 2023 which is 9 weeks less than the same time last year.

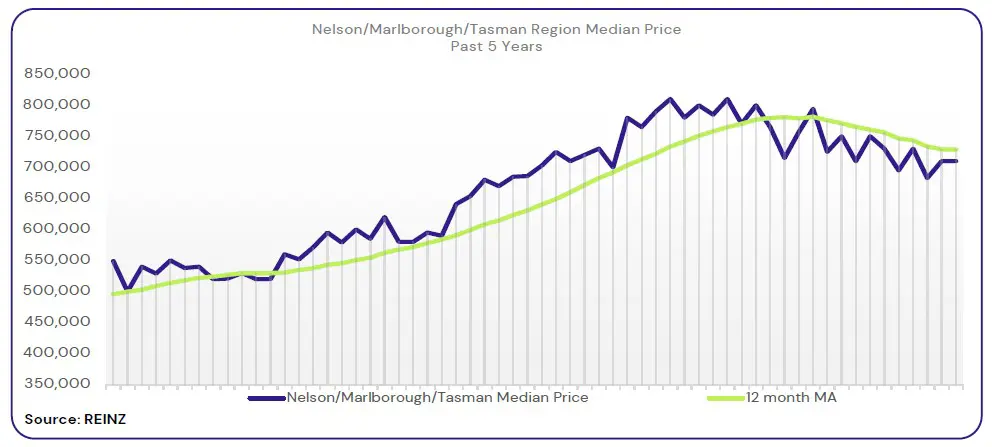

Median prices in Nelson increased by 0.7% year-on-year to $685,000. In Marlborough, median prices decreased by 9.0% year-on-year to $610,000. In Tasman, median prices decreased by 2.9% year-on-year to $782,000.

“Owner-occupiers were the most active in Blenheim and Nelson, with first-home buyers also being fairly active in Nelson. Some vendors have adjusted their price expectations to current market values in Nelson, while vendor expectations rose in Blenheim as more multi-offers are occurring in the area.

Open-home attendance increased slightly across the region.

Cost of living, interest rates, and anticipation of the election continue to play a major role in the decisions of buyers and vendors. While there has been some activity, local salespeople predict that the market will stay the same for the coming months.” (REINZ)

The current median Days to Sell of 55 days is much more than the 10-year average for August which is 39 days. There were 25 weeks of inventory in August 2023 which is 2 weeks more than the same time last year.

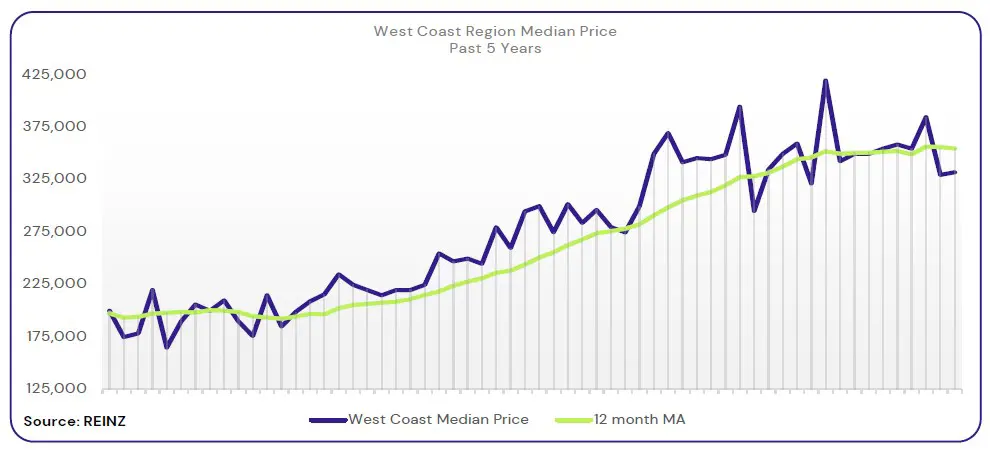

The West Coast’s median prices decreased by 5.0% year-on-year to $332,389.

“August was a quiet month for real estate on the West Coast. The market was stable throughout the month, which may be a sign that it’s preparing to pick up after the election.

Having received favourable commentary recently on its exceptional value for purchasers and borrowers, local salespeople are quietly confident of the market lifting as we head into spring.” (REINZ)

The current median Days to Sell of 51 days is much less than the 10-year average for August which is 94 days. There were 29 weeks of inventory in August 2023 which is 9 weeks less than the same time last year.

In Canterbury, median prices increased by 0.8% year-on-year to $655,000.

“Owner-occupiers were most active across the region. Local salespeople reported signs of first-home buyers returning in Ashburton, interest from out-of-town buyers in Timaru, and Christchurch saw an increase in buyers across the board. Price expectations for most vendors remained the same, however, some vendors in Christchurch achieved better prices.

Overall attendance for open-homes increased, thanks to the improving weather and new listings in Christchurch.

Auction room attendance rose in Timaru and Christchurch with some sales happening in Timaru. For sales counts, August proved slightly busier for Ashburton and Timaru.

Factors like interest rates, cost of living and the election still affect the market. Local agents report that some buyers are waiting for the right opportunity.” (REINZ)

The current median Days to Sell of 34 days is the same as the 10-year average for August which is 34 days. There were 15 weeks of inventory in August 2023 which is 1 week less than the same time last year.

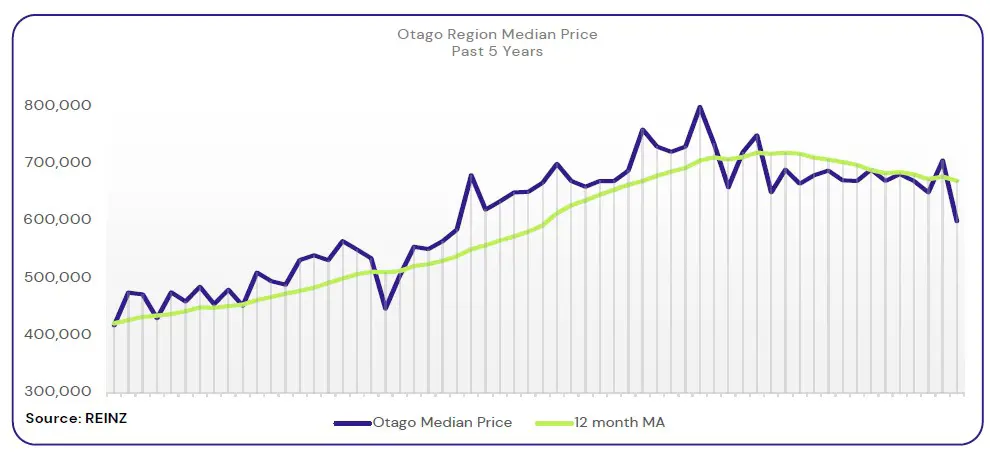

Dunedin City - In Dunedin, the median price decreased by 7.5% year-on-year to $555,000.

“There was a welcome increase in activity in the Dunedin market with 161 sales in August, up 33% from 121 in July.

The bulk of activity was in the mid-to-lower value range, which was reflected in the median price of $555,000. This is down on recent months but in keeping with the trend of the past year. Stock levels are still low, and this is being amplified by the stronger buyer activity.” (REINZ)

Queenstown Lakes “First-home buyers and owner-occupiers were still the most active buyers. Prices among vendors remained steady, with some willing to move while others waited for more favourable conditions. Attendance at open homes remained steady. Auctions remained the best option for buyers and sellers.

Local agents report a short supply of listings and low sales counts. Agents also say that the market is showing signs of sales numbers increasing, and there are signs that factors influencing the market will become steadier. Factors such as interest rates, and anticipation of the coming election continue to affect choices. However, confidence in the market continues to grow and there is a general feeling of optimism as the number of buyers moving into the area continues to be strong.” (REINZ)

The current median Days to Sell of 47 days is much more than the 10-year average for August which is 35 days. There were 17 weeks of inventory in August 2023 which is 2 weeks more than the same time last year.

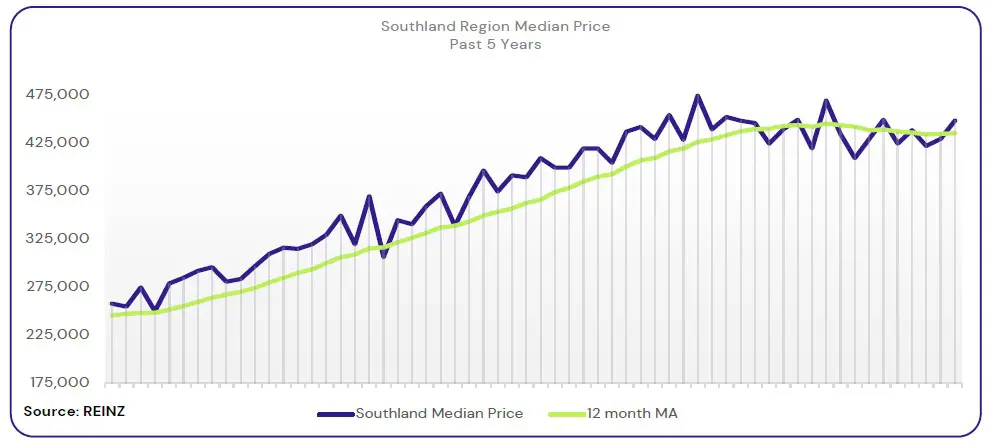

In Southland, median prices increased by 2.0% year-on-year to $449,000.

“There was a slight increase in interest among all buyer groups in August.

Local agents reported that vendor expectations were stable across the region. There was a slight increase in attendance and activity in both open homes and auction rooms. However, the majority of sales were still by private treaty.

The improving weather has had an impact on the market. Overall, there appears to have been an increase in market activity and a slight improvement across the region, with local agents reporting more transactions and more optimism for the future. Anticipation of the upcoming election is also playing a role on market sentiment.” (REINZ)

The current median Days to Sell of 44 days is more than the 10-year average for August which is 37 days. There were 21 weeks of inventory in August 2023 which is 6 weeks more than the same time last year.

From the top of the North through to the deep South, our salespeople are renowned for providing exceptional service because our clients deserve nothing less.

Managing thousands of rental properties throughout provincial New Zealand, our award-winning team saves you time and money, so you can make the most of yours.

With a team of over 850 strong in more than 88 locations throughout provincial New Zealand, a friendly Property Brokers branch is likely to never be too far from where you are.